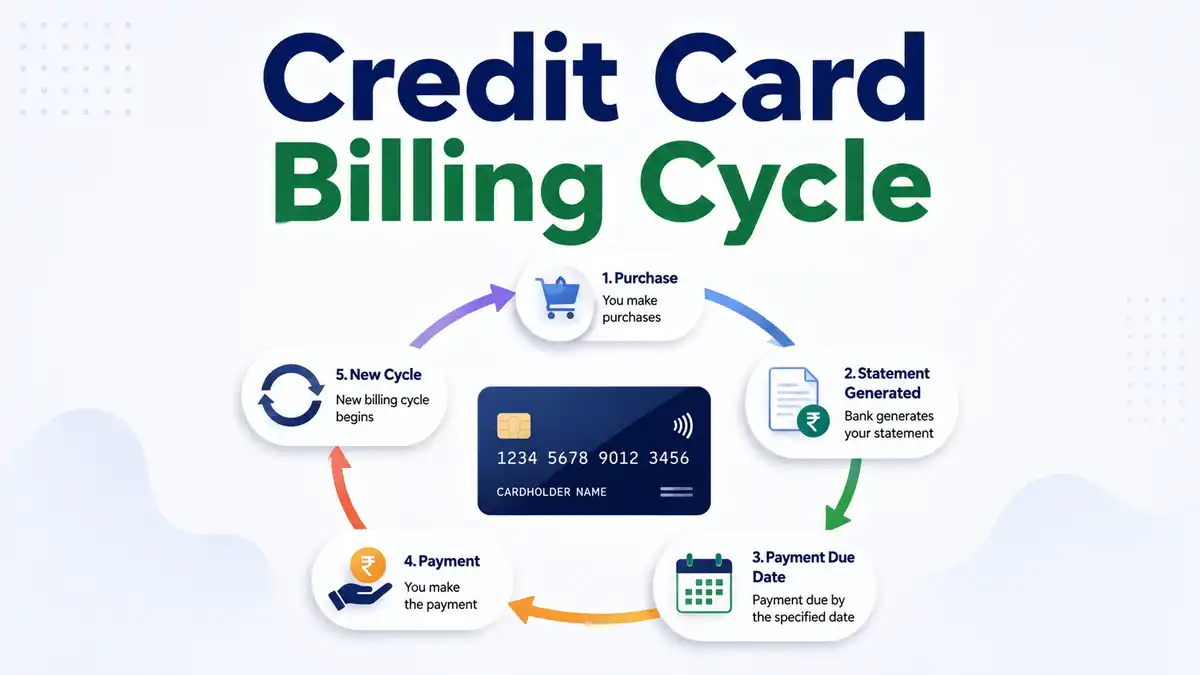

A credit card billing cycle is the period when all your credit card spending is tracked before your bill is created. You keep using your card for everyday things like shopping, food, travel, or online payments, and everything gets recorded during this time. At the end of this period, the bank adds all your transactions together, prepares a single statement, and tells you how much you need to pay and by when.

Understanding the billing cycle helps you know when your bill is generated, when payment is due, and how much time you have to pay. It can also help you avoid late fees and use your credit card wisely.

In this guide, we will explain the credit card billing cycle in simple words with examples and practical tips for Indian users.

Credit Card Billing Cycle Explained With Example

A credit card billing cycle, also called a billing period, statement cycle, or monthly statement period, is the fixed time between two credit card statement dates. It usually lasts around 28 to 31 days. During this period, your bank records all card transactions like shopping, online payments, EMI purchases, cash withdrawals, charges, fees, and refunds.

At the end of the cycle, the card issuer generates your credit card statement or monthly bill with details like total outstanding balance, minimum due amount, available credit limit, and payment due date.

Let’s Understand With an Example

Suppose your billing cycle is from 5th January to 4th February. If you spend on 7th January, 11th January, 20th January, or even 2nd February, all these transactions will be added together in the bill generated on 4th February. So instead of seeing each payment separately, everything is grouped into one statement based on your cycle.

How Credit Card Billing Cycle Works

The billing cycle is the process your bank uses to calculate your monthly bill and payment due date. Understanding how it works can help you manage payments better, avoid late fees, and use the interest-free period wisely.

Key Parts of a Credit Card Billing Cycle:

Transaction Date

The transaction date is the day you use your credit card to make a payment.

For example, if you buy shoes on 6 March, then 6 March is your transaction date.

Statement Date

The statement generation date is the day your bank creates your monthly credit card bill or statement. All eligible transactions made during the billing period are added to this bill.

For example, if your statement date is 5 April, then purchases made before that date may appear in that month’s statement.

Payment Due Date

The due date is the last date to pay your credit card bill. Most banks give around 15 to 20 days after the statement date.

For example, if the statement date is 5 April, then the payment due date is 22 April.

Total Amount Due

This is the full outstanding amount shown in your credit card statement. Paying the total due on time usually helps you avoid interest charges.

Minimum Amount Due

This is the minimum payment required to keep your account regular for that month. However, paying only the minimum due may lead to interest on the remaining balance.

Interest-Free Period

If you pay your full bill before the due date, you may get an interest-free period on purchases. This can be around 20 to 50 days, depending on your purchase date and card issuer.

Credit Card Billing Cycle Example In India

Now, let’s understand this with a simple example. It will help you see how the billing cycle works and how your monthly spending is added to one credit card bill.

Let’s assume that your billing cycle runs from January 6th to February 5th.

| Date | Transaction | Amount | Included In This Bill? |

|---|---|---|---|

| 8 January | Groceries | ₹1,500 | Yes |

| 14 January | Fuel | ₹3,500 | Yes |

| 22 January | Mobile Purchase | ₹10,000 | Yes |

| 3 February | Food Order | ₹2,000 | Yes |

| 6 February | Movie Tickets | ₹2,500 | No (Next Bill) |

- Your Statement Date: 5 February

- Your Total Bill: ₹17,000

- Your Due Date: Around 22 February

What’s happening here?

- 6 Jan to 5 Feb is your billing period

- All expenses during this time (₹17,000) are added to one bill

- Any spend after 5 Feb (like 6 Feb) will come in the next bill

Simple takeaway

If you understand your billing cycle, you can:

- Know the best time to spend

- Understand which expenses will come in which bill

- Get more interest-free time

Simple rule: Spend after the statement date = more time to pay

Billing Date vs Statement Date vs Due Date

At first, these can feel a bit confusing, especially if you’re new to using a credit card. But once you understand them, everything becomes much easier. They simply explain three things: first, when your monthly spending is counted, second, when your bill is created, and third is how much time you get to pay it. We will understand all of this in simple terms below.

What is Billing Date

The billing date is the last day of your billing cycle. On this day, your bank stops counting your monthly transactions and prepares your bill.

In most cases, the billing date and statement date are the same thing.

What is the Statement Date

The statement date is the day when your credit card statement (bill) is generated. It shows all your transactions, the total bill, and payment details.

Simply put, this is the day you receive your monthly bill.

What is the Due Date

The due date is the last date to pay your credit card bill. You usually get 15 to 20 days after the statement date to make the payment.

Paying on or before this date helps you avoid late fees and interest charges.

Difference Table

| Term | It's Meaning | Why it matters |

|---|---|---|

| Billing Date | Last day of your billing cycle | Transactions after this go to next bill |

| Statement Date | The day your bill is generated | Shows your total amount due |

| Due Date | Last date to pay the bill | Avoid late fees and interest |

Simple understanding

- Billing Date = Cycle ends

- Statement Date = Bill is created

- Due Date = Last day to pay

Once you understand this, it will become much easier to manage your credit card and avoid extra charges.

How Many Days Is a Credit Card Billing Cycle?

Your credit card billing cycle usually lasts 28 to 31 days, which is almost like one month.

In simple terms, this is the period when your bank tracks all your spending and adds it to a single bill. Once this period ends, your statement is generated, and a new cycle starts from the next day.

For example, if your billing cycle starts on the 10th of a month, it will usually end on the 9th of the next month. All the purchases you make during these days will come in one bill.

So, you can think of it like a simple monthly routine, your spending is recorded for about 30 days, then your bill is created, and the cycle starts again.

Best Time to Use a Credit Card for Maximum Free Days

As you can see in the image, if you want to get the most out of your credit card, timing your spending matters a lot. The best time to use your credit card is just after your statement date.

This is because a new billing cycle starts right after the statement is generated. So, any purchase you make at this time will be added to the next month’s bill, giving you the maximum time to repay. In many cases, this can give you around 45 to 50 days of interest-free time.

On the other hand, if you spend just before your statement date, that amount will appear in the current month’s bill, and you will get much less time to pay.

So, a simple habit can make a big difference. Try to use your card right after your statement is generated.

How to Check Your Credit Card Billing Cycle Online

If you are not sure about your billing cycle, you can easily check it online. Most banks clearly show your statement date and due date, which helps you understand your cycle.

You can find these details in your mobile banking app, net banking account, or your monthly statement PDF.

For SBI Card User

If you are using an SBI credit card, open the SBI Card mobile app or log in to your account online. Go to the “My Account” or “Statements” section. There, you will find your statement date, due date, and recent transactions.

You can also check details here: SBI Card

For HDFC Bank User

For HDFC credit card users, log in to the HDFC Bank app or net banking. Go to the “Cards” section and open your credit card details. Your billing cycle, statement, and due date will be clearly visible there.

Official page: HDFC Bank

For ICICI Bank User

If you have an ICICI credit card, open the iMobile app or net banking. Go to the credit card section and check your statement details. You will find your billing cycle information there.

Official page: ICICI Bank

A simple tip: if you ever feel confused, just download your latest statement. It shows everything clearly in one place.

Can You Change Your Billing Cycle Date?

Yes, in many cases, banks do allow you to change your billing cycle date. This can be useful if you want to match your credit card due date with your salary date or cash flow.

You can request this change through customer care, net banking, or your bank’s mobile app. However, banks usually have some conditions. You may not be able to change it frequently, and sometimes one billing cycle may get adjusted during the change.

So, it’s possible, but it depends on your bank’s rules.

Does Billing Cycle Affect Your Credit Score?

Your billing cycle does not directly affect your credit score, but it plays an important role in how your usage is reported.

For example, the amount shown in your statement is what gets reported as your credit usage. If your spending is very high during the cycle and reflected in your statement, it can increase your credit utilization, which may impact your CIBIL score.

Also, if you miss your payment due date, it can negatively affect your credit score. On the other hand, paying your full bill on time helps build a good credit history.

So, while the billing cycle itself is just a timeline, how you manage it makes a real difference.

5 Billing Cycle Mistakes That Cost You Money

Many people lose money on credit cards simply because they do not fully understand the billing cycle.

These are common mistakes many people make, and they end up paying extra money without realizing it:

1. Missing the due date

If you don’t pay on time, the bank charges a late fee and interest. This can increase your bill quickly.

2. Paying only the minimum Due amount

Paying only the minimum due amount on your credit card, It may look safe, but the remaining balance starts getting high interest. This can turn into a big amount over time.

3. Spending heavily just before the statement date

This gives you very little time to repay because the amount comes in the current bill.

4. Not understanding your billing cycle

If you don’t know your cycle, you may get confused about which expense will come in which bill.

5. Not paying the full bill

If you don’t pay the total amount, you lose the interest-free benefit, and credit card interest gets added.

Simple rule: Understand your billing cycle, always pay the full amount, and never miss the due date.

Avoiding these small mistakes can save you a significant amount of money over time.

Credit Card Billing Cycle FAQs

1. Is the billing date the same as the statement date?

In most cases, yes. The statement date is usually the last day of your billing cycle.

2. How long is a billing cycle?

It is usually between 28-31 days, depending on your bank.

3. How to use a credit card for maximum benefit?

Right after your statement date, so you get more time to repay.

4. Is paying the minimum due enough?

It avoids penalties for that month, but interest will be charged on the remaining amount.

5. Can I change my billing cycle?

Yes, some banks allow it, but it depends on their policies.

The Final Thought

A credit card billing cycle is simply a monthly system that tracks your spending, generates your bill, and gives you time to repay it. Once you understand how this billing cycle works, using a credit card becomes much easier and more controlled.

Instead of guessing when your bill will come or how much time you have, you can plan your spending, choose the right time to use your card, and make payments without stress.

Over time, this not only helps you avoid unnecessary charges but also builds better financial discipline. A small understanding of your billing cycle can make a big difference in how you manage your credit card.

Disclaimer

This article is for educational purposes only. Credit card features, charges, and policies may vary depending on the bank. Always check your bank’s official terms and conditions before making financial decisions.